What is a Medicare Supplement?

Medicare Supplements, also known as Medigap is a supplemental insurance you can get on top of your Medicare Parts A & B. Medicare covers many healthcare costs, but it does not pay for every expense. You are responsible for these costs, sometimes called the “gaps” in Medicare coverage. Medigap helps pay for the gaps, much like retiree insurance.

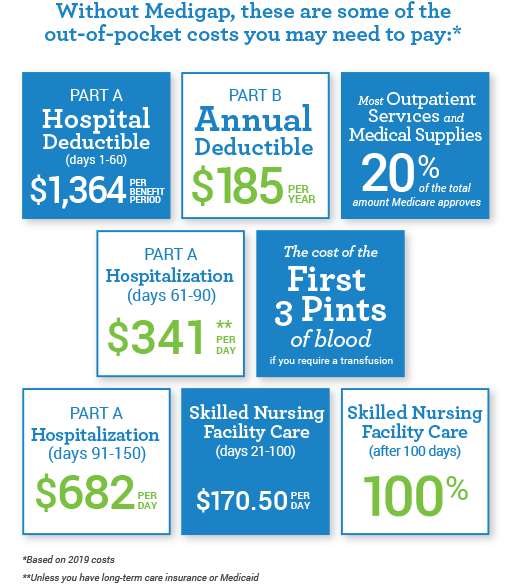

What are the gaps in Medicare coverage?

How does Medigap work?

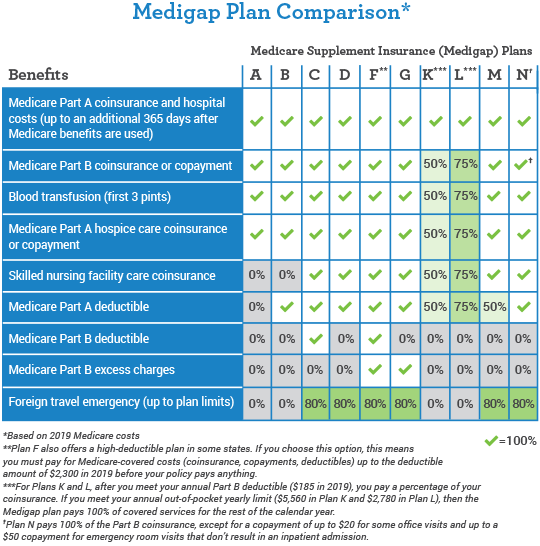

You can buy Medigap from private insurance companies in your state. There are 11 different standard Medigap plans that can be sold in most states. The 11 standard plans are labeled A-D, F, high-deductible F, G and K-N. Each of these plans covers different services.

What doctors can I see with Medigap?

With Medigap, you can see any doctor, whether the doctor accepts Medicare assignment or not.

If your doctor “accepts assignment,” meaning he or she agrees to be paid the Medicare-approved amount for a service, your Medigap insurance company usually pays your doctor directly.

If your doctor does not accept Medicare assignment, you may have to send claims to your insurance company and pay the doctor yourself.

Note, however, that Medigap plans generally do not pay for care received outside of the United States, except for medically necessary emergency care that occurs during the first 60 days of your trip.

What are my rights with Medigap?

People who purchase a Medigap policy have certain rights:

Free look periods

Guaranteed issue rights

Renewals

These rights can protect you from being denied coverage. They also can protect you from having to keep a plan that is not right for you.

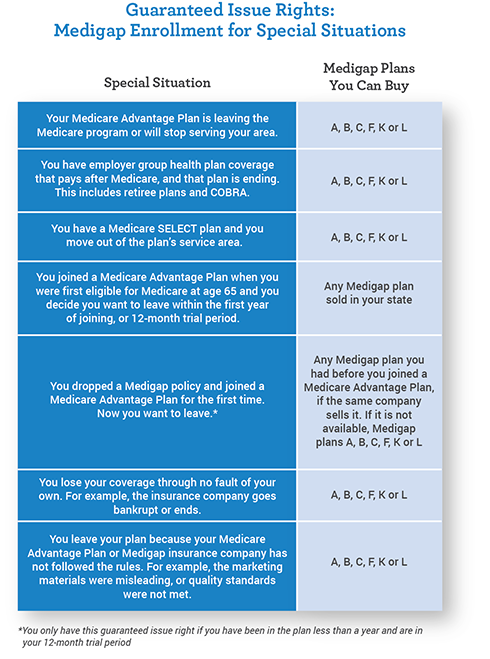

Guaranteed Issue Rights

In some situations, you have the right to buy a Medigap policy outside of your Medigap Open Enrollment Period. These rights are called “Medigap protections” or guaranteed issue rights because the law says that insurance companies must sell or “issue” you a Medigap policy even if you have health problems. And this way, if you lose your current insurance, such as coverage through your job or a Medicare Advantage plan, you get the chance again to buy a Medigap policy.

In most cases, you must buy your new Medigap plan within 63 days of the time your previous health coverage ends. In these cases, you will not have to wait to get covered.

Selling Medicare Supplements

It’s important to understand that Medicare Supplements can be sold at any time of the year WITHOUT many of the limitations or oversight as with Medicare Advantage. Outside of the Medicare Open Enrollment Period plans are fully underwritten, very similar to Final Expense. Even though the plans are standardized (Plan G with company A is exactly the same as Plan G with company B), underwriting and price can vary significantly.

*Medigap does NOT cover prescription drugs and therefore the beneficiary will need to sign up for a stand-alone PDP.